Quant Next

The Cox-Ross-Rubinstein Binomial Option Pricing Model

3 years ago - 6:22

SkillFine

How to Find The Right Price of a Stock Option Using Binomial Option Pricing Model

11 months ago - 1:02

Stock Station

Binomial Tree - Super Stocks Market Concepts

5 years ago - 0:10

julia’s algos

Option Pricing Models NO ONE Talks About #shorts

3 months ago - 0:59

Mathematics

Unlocking Stock Options Pricing Secrets!

11 months ago - 0:26

Brian Byrne

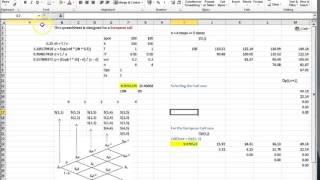

Simple Introduction to Cox, Ross and Rubinstein (1979) 2

7 years ago - 15:02

Brian Byrne

Cox, Ross and Rubinstein (1979) with Dividends

7 years ago - 14:05

Brian Byrne

Simple Introduction to Cox, Ross and Rubinstein (1979) 3

7 years ago - 14:59

Zen Trader

Option Pricing Made Simple: The Black-Scholes Model Demystified

11 months ago - 1:58

DevM2od

Binomial Model: Easy Option Pricing Steps

7 months ago - 1:02

Risk Hub

A tiny change in volatility can move markets by billions 💸 | CFA, Risk & Quant Finance Insights 🚀”

4 months ago - 0:40

Brian Byrne

VBA Static Code for estimating Options on Futures using a Cox, Ross and Rubinstein tree

5 years ago - 5:20

mbacalculator

MBACalculator.com - Cox Ross Rubenstein Binomial Option Pricing Model

16 years ago - 5:07

Mathe Mannheim

Mathematical Finance L 10-1: Cox-Ross-Rubinstein model

4 years ago - 49:37

Brian Byrne

Simple Introduction to Cox, Ross Rubinstein (1979) 1

7 years ago - 15:02

PrepNuggets

CFA Level I Derivatives - Binomial Model for Pricing Options

5 years ago - 5:31

Brian Byrne

From Static to Dynamic Binomial Tree 2

7 years ago - 14:54

Brian Byrne

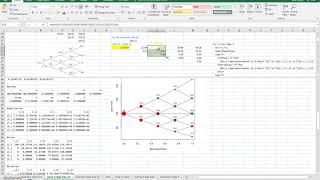

Introduction to a simple Cox Ross Rubinstein Binomial Tree 4

10 years ago - 14:59

Brian Byrne

Cox, Ross and Rubinstein, Tian, Jarrow-Rudd and Leisen-Reimer convergence to True - R in Excel

4 years ago - 38:51

Brian Byrne

American Option Visualisation in the R derivmkts package 2

6 years ago - 10:36

Brian Byrne

Cox Ross Rubinstein VBA Fabrice Rouah

5 years ago - 4:50

Brian Byrne

Introduction to a simple Cox Ross Rubinstein Binomial Tree 1

10 years ago - 15:01

QuantPy

How to Choose Binomial Parameters - Binomial Option Pricing || Theory & Implementation in Python

4 years ago - 17:28

Brian Byrne

C++ Xcode Cox Ross Rubinstein for 4 step tree

10 years ago - 4:13

Brian Byrne

Valuation of futures options using binomial trees 2

6 years ago - 14:55

Brian Byrne

Leisen Reimer and Cox, Ross and Rubinstein estimation for Binary Options

5 years ago - 17:24

Brian Byrne

Cox Ross and Rubinstein and Jarrow Rudd in Python Jupyter Notebook

6 years ago - 11:58

Brian Byrne

Speeding up the Dynamic Binomial tree 2

7 years ago - 15:02

Brian Byrne

Python Code for Cox Ross and Rubinstein evaluating American Options

5 years ago - 11:06

Brian Byrne

Python Code for Cox Ross and Rubinstein implemented in Spyder using Espen Haug approach

5 years ago - 4:59

Brian Byrne

Cox Ross Rubinstein implemented in Xcode C++ (from Volopta Leisen Reimer)

10 years ago - 5:41

![The Binomial Model [Lox-Ross-Rubenstein Model]](/vi/9wDtbThIZSM/mqdefault.jpg)