Quant Next

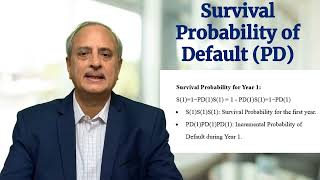

Credit Risk Modelling: The Probability of Default

1 year ago - 7:54

Roman Davydov

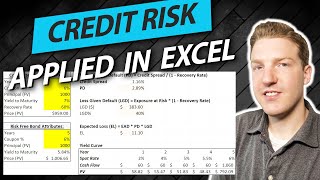

3. Expected loss EL and its components PD LGD and EAD

1 year ago - 4:13

Bionic Turtle

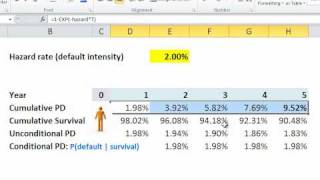

Conditional default probability (hazard rate)

15 years ago - 8:02

RAFAEL CASTILLO-TRIANA

PROBABILITY OF DEFAULT- WEBINAR 2: WHAT IS DEFAULT? WHAT IS PROBABILITY?

3 years ago - 51:52

The Friendly Statistician

How To Calculate Probability Of Default From CDS Spread? - The Friendly Statistician

9 months ago - 4:35

Roman Davydov

48. Calculating probability of default for a single customer

1 year ago - 4:32

Bionic Turtle

Cumulative probability of default on risky bond

17 years ago - 8:18

Data Engineering Toolbox

Credit Risk Analysis Series: Calculating Probability of Default (PD) with Databricks and PySpark

1 year ago - 8:26

Learnerea

Credit Risk - Probability of Default, End-to-End Model Development | Beginner to Pro Level

3 years ago - 1:10:37

CQF Institute

Understanding Default Probability - Dr. Alonso Peña's Insights in Quant Finance

1 year ago - 7:27

Bionic Turtle

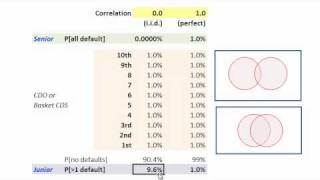

Default correlation in CDO or basket CDS

15 years ago - 7:35

finRGB

Understanding Default Correlation | Credit Risk | FRM Part 2

6 months ago - 2:55

Bionic Turtle

FRM: Logistic distribution maps credit score to probability of default (PD)

15 years ago - 8:57

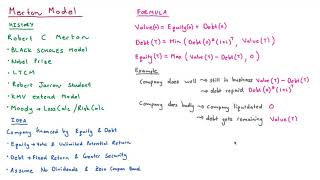

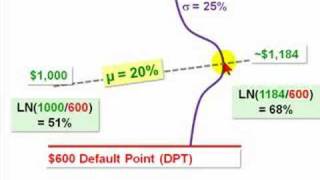

Finuture

Default Probability Using the Merton Model

1 year ago - 20:24

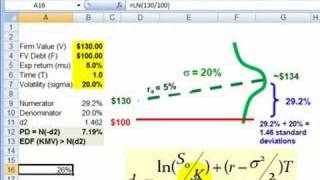

NEDL

KMV model explained: Modelling default risk (Excel)

2 years ago - 17:12

Bionic Turtle

FRM: Expected default frequency (EDF, PD) with Merton Model

17 years ago - 9:29

Bionic Turtle

FRM: How d2 in Black-Scholes becomes PD in Merton model

17 years ago - 10:00

KnowledgeVarsity

Probability of Default Computation Problem - FRM Part 1 and CFA Level 1 Examination

13 years ago - 8:47

Bionic Turtle

FRM: Valuation of credit default swap (CDS)

17 years ago - 9:25

finRGB

Real World Vs Risk Neutral Default Probabilities (FRM Part 2, Book 2, Credit Risk)

6 years ago - 9:49

AnalystPrep

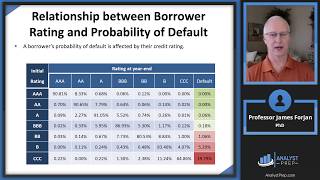

Rating Assignment Methodologies (FRM Part 2 2025 – Book 2 – Chapter 4)

5 years ago - 54:28

RAFAEL CASTILLO-TRIANA

EPISODE 7- PROBABILITY OF DEFAULT- CALCULATING PROBABILITY OF DEFAULT

2 years ago - 1:22:27

Quant Next

Credit Risk Modelling: Default Time Distribution

1 year ago - 5:09

finRGB

Hazard Rate / Default Intensity and its Interpretations (FRM Part 2, Book 2, Credit Risk)

7 years ago - 14:21