ritvikmath

GARCH Model : Time Series Talk

6 years ago - 10:25

Aric LaBarr

What are ARCH & GARCH Models

3 years ago - 5:10

Roman Paolucci

Master Volatility with ARCH & GARCH Models

3 months ago - 48:05

ritvikmath

Time Series Talk : ARCH Model

6 years ago - 10:29

ritvikmath

Coding the GARCH Model : Time Series Talk

5 years ago - 10:08

Patrick Boyle

Time Varying Volatility and GARCH in Risk Management

6 years ago - 6:23

NEDL

GARCH model - volatility persistence in time series (Excel)

5 years ago - 22:22

ritvikmath

Stock Forecasting with GARCH : Stock Trading Basics

5 years ago - 7:26

Professor Rahul Jain

GARCH vs ARIMA Explained | Which Time Series Model Should You Use?

7 months ago - 2:54

Bionic Turtle

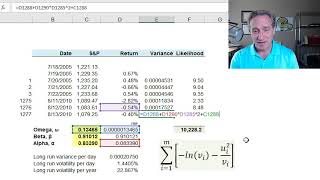

Maximum likelihood estimation of GARCH parameters (FRM T2-26)

7 years ago - 12:12

Bionic Turtle

Volatility: GARCH 1,1 (FRM T2-23)

7 years ago - 14:45

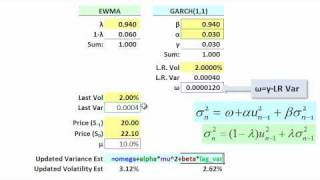

Bionic Turtle

FRM: EWMA versus GARCH(1,1) volatility

15 years ago - 9:55

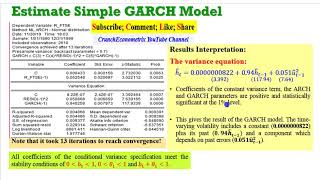

CrunchEconometrix

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlm

6 years ago - 14:25

Roman Paolucci

Modeling Volatility with ARCH & GARCH

3 months ago - 0:52

Learn About Economics

How Does The GARCH Model Predict Volatility? - Learn About Economics

6 months ago - 3:11

C-RAM

Basics of ARCH-GARCH Modeling

6 years ago - 3:52

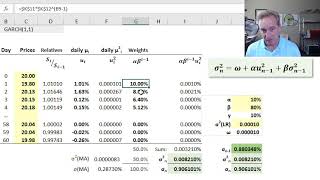

Bionic Turtle

FRM: GARCH(1,1) to estimate volatility

17 years ago - 7:52

NEDL

GARCH in mean (GARCH-M) model: volatility persistence and risk premia (Excel)

4 years ago - 17:46

Md Sihab Sarar

Gold Returns Volatility Forecasting | GARCH vs Deep Learning | MSc Statistics Project

8 months ago - 10:19

Bionic Turtle

Forecast volatility with GARCH(1,1) (FRM T2-24)

7 years ago - 9:44

bruno v

OM 12: Introduction to GARCH(1,1)

5 years ago - 41:51

C-RAM

Do S&P 500 Returns follow an GARCH? Working on that, we learn how to estimate a GARCH from scratch

4 years ago - 5:32

finRGB

GARCH (1,1) Volatility Model: A Closer Look | FRM Part 1 | Book 4 | Valuation and Risk Models)

7 years ago - 21:30