We are a boutique financial service firm specializing in quantitative analysis, derivatives valuation and risk management. We combine the power of traditional structured finance with modern high performance computing in order to deliver unique solutions to our customers. Our clients range from asset management firms to industrial, non-financial companies. Our services include:

#derivative #valuation #accounting

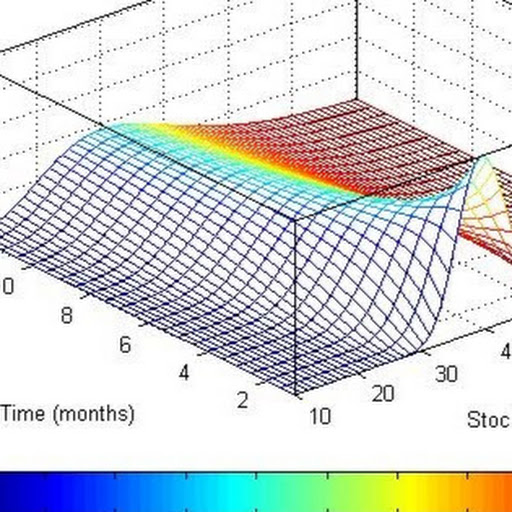

DERIVATIVE VALUATION

Valuation of financial derivatives such as convertible bonds, mortgage backed securities, variance swaps, credit default swaps, collateral debt obligation

Development of Monte Carlo valuation model to value executive stock options and real options

Yield curve construction (LIBOR, overnight index swap, cross currency) in various currencies

Development of a structural credit model for determining corporate credit spreads and probabilities of default

Implementation of advanced derivative pricing models

Independent Price Verification

General derivative valuation services

RISK MANAGEMENT

Risk analytics for derivatives books such as calculation of the Greeks, Value at Risk

Validation of risk management models such as Economic Capital, IFRS9

Implementation of advanced options pricing models: stochastic volatility, local volatility

Development of multi-factor stochastic models for volatility and commodity related products

Design and implementation of database for financial data and analytics

Developing trading and hedging strategies for equity and commodity portfolios

General quantitative analysis services

tech.harbourfronts.com/contact/

Harbourfront Technologies

Harbourfront Technologies

コメント