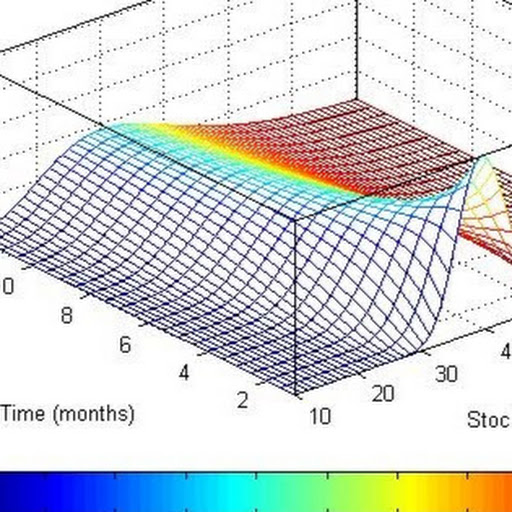

In this post, we focus on the implementation of the Black-Scholes-Merton option pricing model in Python. Closed-form formula for European call and put are implemented in a Python code. We compare the results to the ones obtained by using third-party software and notice that they are in good agreement.

#python #derivative #excel

tech.harbourfronts.com/derivatives/black-scholes-m…

Harbourfront Technologies

Harbourfront Technologies

コメント